Blockchain technology has been making waves in the tech world for years now, and with the rise of cryptocurrencies like Bitcoin, it has become more important than ever to understand the basics of blockchain. While there is a lot of information available on this topic, it can be overwhelming and confusing for those who are just starting to learn about it. In this guide, we will break down the concept of blockchain and provide a comprehensive overview of blockchain info, including its benefits, misconceptions, and applications.

Introduction to Blockchain

Before diving into the specifics of blockchain info, it is essential to have a solid understanding of what blockchain is and how it works.

What is Blockchain?

At its core, blockchain is a decentralized, transparent, and secure digital ledger that records transactions between two parties efficiently and permanently. It is made up of blocks of data, where each block is linked to the previous one, forming an unalterable chain. This chain of blocks is distributed across a network of computers, making it nearly impossible to tamper with or manipulate the data stored within it.

The most significant advantage of blockchain is its decentralized nature. Unlike traditional systems where a central authority controls and verifies transactions, blockchain relies on a network of nodes (or computers) to validate and add new blocks to the chain. This decentralization eliminates the need for intermediaries, making transactions faster, cheaper, and more secure.

How Blockchain Works

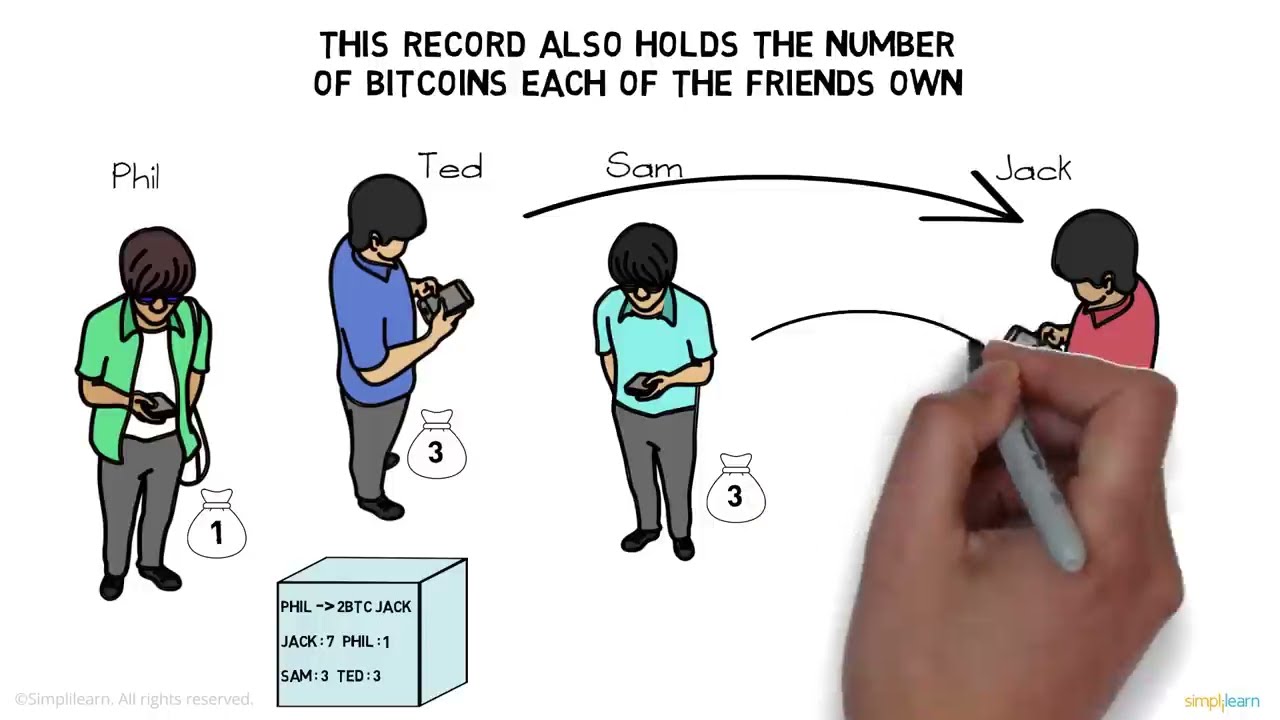

To understand how blockchain works, let’s imagine a scenario where Alice wants to send money to Bob through a traditional bank transfer. Here’s what happens:

- Alice initiates a transfer request to her bank.

- Her bank verifies her identity and account balance.

- The bank debits Alice’s account and credits Bob’s account.

- The transaction is recorded in the bank’s database.

- Bob receives the money after the bank deducts its fees.

This process involves multiple intermediaries (e.g., banks, payment processors) and can take days to complete. Moreover, the information related to the transaction is stored in a centralized database, making it vulnerable to hacks and manipulation.

Now, let’s see how blockchain simplifies this process:

- Alice initiates a transfer request by creating a digital signature using her private key.

- The network of nodes verifies the validity of the transaction using specialized algorithms.

- Once validated, the transaction is added to a block.

- The block is then distributed to all the nodes in the network.

- New blocks are added to the chain, forming an immutable record of transactions.

- Bob receives the money almost instantly, with little to no fees involved.

As you can see, the absence of intermediaries and the distributed nature of blockchain make the process more efficient, secure, and transparent.

Benefits of Blockchain Technology

The potential benefits of blockchain technology are immense, and they extend beyond just financial transactions. Let’s look at some of the key advantages of utilizing blockchain.

Decentralization

As mentioned earlier, blockchain technology operates on a decentralized network, meaning there is no need for a central authority or middlemen to validate and store data. This level of decentralization eliminates the risk of a single point of failure and ensures that there is no single entity controlling the network. It also reduces the likelihood of human error and manipulation, making blockchain a highly reliable system.

Immutability

Since each block in the blockchain is linked to the previous one, tampering with data becomes incredibly challenging. Any attempt to modify a block would require altering all subsequent blocks on the chain, which is nearly impossible due to the complex cryptographic algorithms used to keep the network secure. This immutability makes blockchain a perfect solution for industries where data integrity is critical, such as healthcare, supply chain management, and voting systems.

Transparency

All transactions on a blockchain are recorded on a public ledger that is accessible to all network participants. This transparency ensures that all parties have access to the same data, minimizing the likelihood of fraud and increasing trust between them. Additionally, since every transaction is timestamped and traceable, it provides an audit trail that can be used for record-keeping or dispute resolution.

Cost and Time Efficiency

Blockchain eliminates the need for intermediaries, which translates to significant cost savings for businesses. Moreover, since transactions are automated and do not require manual verification, they can be completed faster than traditional methods. This increased efficiency reduces the time and costs associated with processes like cross-border payments, supply chain tracking, and real estate transactions.

Different Types of Blockchains

There are three main types of blockchains: public, private, and hybrid. Understanding the differences between these types is crucial in comprehending how blockchain info works.

Public Blockchain

A public blockchain is open to everyone, meaning anyone can join the network, verify and add blocks to the chain. A perfect example of this type of blockchain is the Bitcoin network, where miners use computational power to validate transactions and add them to the chain. Since anyone can participate in the process, there is no centralized authority controlling the network, making it truly decentralized.

Private Blockchain

Private blockchains are permissioned networks where only authorized participants can validate transactions and add blocks to the chain. These networks are typically used by enterprises and organizations as they provide more control over the network and its participants, making it easier to comply with regulations and privacy laws.

Hybrid Blockchain

As the name suggests, a hybrid blockchain combines features from both public and private blockchains. In a hybrid blockchain, some parts of the network are open to the public, while others are restricted to authorized users. This type of blockchain is useful in scenarios where transparency is required for some transactions, but privacy is needed for others.

Common Misconceptions about Blockchain

Despite its increasing popularity and adoption, there are still many misconceptions about blockchain technology. Let’s debunk some of the most common ones.

Blockchain is only useful for financial transactions

While blockchain’s first use case was for cryptocurrencies, it has since evolved to be used in various industries such as healthcare, supply chain management, and voting systems. Its decentralized, secure, and transparent nature makes it a valuable tool for any process that requires data integrity and trust between parties.

Blockchain is only for large corporations

Blockchain technology is accessible to anyone with an internet connection, not just large organizations. With the rise of blockchain platforms like Ethereum and NEO, developers can build decentralized applications (DApps) on top of existing blockchains, making the technology more accessible and affordable for small businesses and individuals.

Blockchain is anonymous and untraceable

While blockchain provides a high level of privacy, it is not entirely anonymous. Each transaction is recorded on a public ledger, which means that users’ digital addresses can be traced back to real-world identities. Additionally, the use of smart contracts (self-executing code stored on the blockchain) can reveal information about the parties involved in a transaction.

Applications of Blockchain

The potential applications of blockchain technology are vast, and many industries are currently exploring its use cases. Here are some of the most prominent applications of blockchain.

Cryptocurrencies

Cryptocurrencies are digital assets that use blockchain technology to record and verify transactions. Bitcoin, Ethereum, and Litecoin are some examples of popular cryptocurrencies that have gained mainstream adoption. The decentralization, security, and efficiency of blockchain make it an ideal platform for creating and managing digital currencies.

Supply Chain Management

Blockchain can play a crucial role in supply chain management by providing transparency and traceability throughout the entire process. By recording each stage of the supply chain on the blockchain, companies can track the origin of products, detect counterfeit goods, and ensure ethical and sustainable practices.

Healthcare

Blockchain can transform the healthcare industry by providing a secure and transparent platform for storing medical records. These records can be accessed by authorized parties, making it easier to share patient information while maintaining privacy. Additionally, blockchain-based solutions can be used to track pharmaceutical supply chains and prevent the distribution of counterfeit drugs.

Voting Systems

Blockchain can also revolutionize the way we vote by providing a transparent and secure platform for casting and counting votes. By recording each vote on the blockchain, election results can be verified and audited, ensuring that the process is fair and void of any tampering.

Understanding Blockchain Info

Blockchain.info is a popular website that provides real-time data and statistics related to the Bitcoin network. It offers various services such as a Bitcoin wallet, market charts, and transaction tracking. Here’s a breakdown of some of the key features of Blockchain.info.

Bitcoin Wallet

The Bitcoin wallet from Blockchain.info allows users to store, send, and receive Bitcoins securely. It uses two-factor authentication, multi-signature wallets, and backup encryption to ensure the safety of user funds.

Market Charts and Statistics

Blockchain.info provides real-time market data, including price charts, trade volume, and mining difficulty. Users can also view the number of transactions per day, the average transaction value, and the total number of Bitcoins in circulation.

Transaction Tracking

One of the most useful features of Blockchain.info is its ability to track transactions on the Bitcoin network. Users can enter a transaction ID or address and get details about its status, including the time, value, and confirmation status.

Resources for Learning More about Blockchain

If you’re interested in learning more about blockchain technology, there are plenty of resources available online. Here are some of the best places to start:

- Blockchain Basics Course on Coursera: This course offers a comprehensive introduction to blockchain and its use cases. It covers topics such as decentralization, consensus algorithms, smart contracts, and more.

- Blockchain Revolution by Don Tapscott and Alex Tapscott: This book provides a comprehensive overview of blockchain technology and its potential impact on different industries. It’s an excellent resource for those looking to dive deep into the subject.

- Blockchain.info Blog: The official blog of Blockchain.info offers regular updates and analysis on the latest blockchain trends and news. It also has tutorials and educational articles for beginners.

- Reddit Cryptocurrency and Blockchain Subreddits: Reddit is a great place to engage with the blockchain community and stay updated on the latest developments in the industry. Some popular subreddits include r/Cryptocurrency, r/Bitcoin, and r/Ethereum.

Conclusion

Blockchain is a disruptive technology that has the potential to transform industries and revolutionize the way we conduct transactions. Its decentralized, secure, and transparent nature makes it a perfect solution for various processes that require trust and data integrity. With the rise of blockchain-based applications and platforms, it’s clear that this technology is here to stay. By understanding the basics of blockchain and staying up-to-date with the latest advancements, you can position yourself at the forefront of this exciting and ever-evolving field.